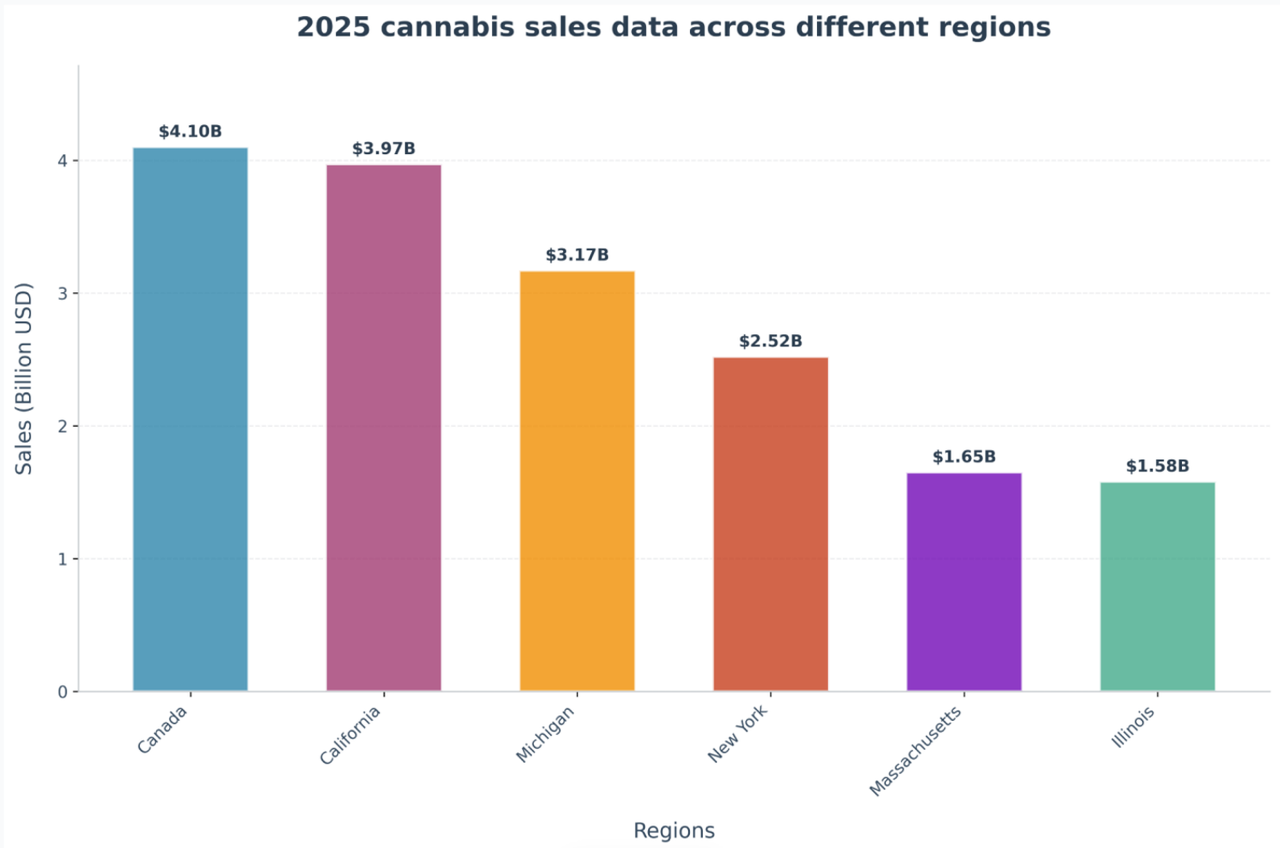

The legal cannabis industry just hit a number that surprised even the insiders. Canada's white market is now bigger than California's. If you're in this business and you're not watching Canada closely, you're missing the picture.

Canada's total cannabis sales reached $4.1 billion USD in 2025, slightly ahead of California's $3.98 billion. Ontario leads all provinces at roughly 40% of national sales. Alberta, British Columbia, and Quebec together account for another 40%-plus of the market.

I've been tracking this market for a while, and one thing stands out: the structure of this market is cleaner than most people think. The sales are concentrated by province, and the product categories are concentrated too. That makes it easier to know where the real action is. Let me break it down.

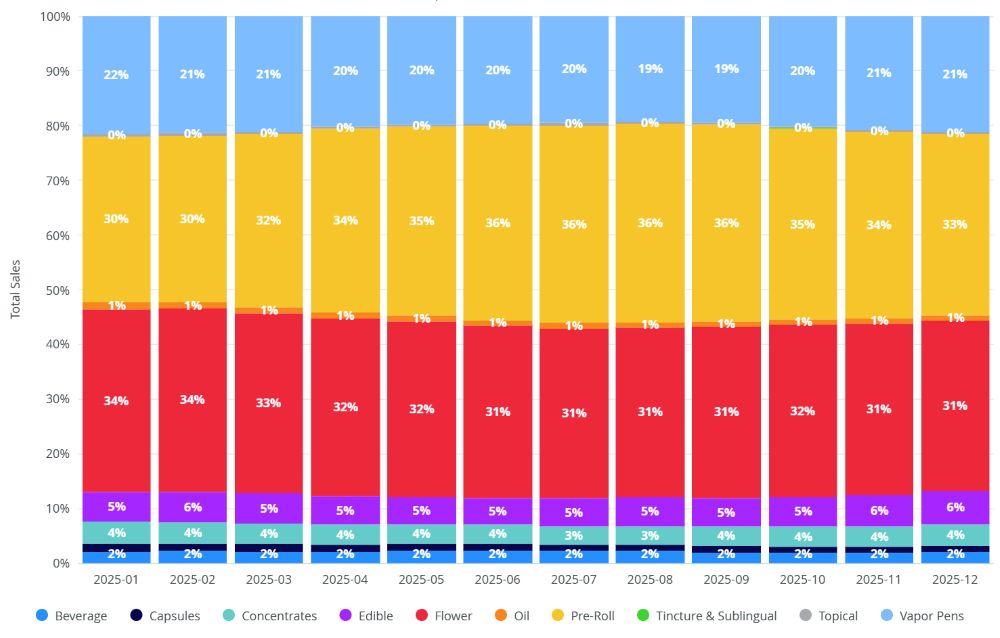

Which Cannabis Product Types Are Winning in Canada in 2025?

Three categories dominate, and everything else fights over the scraps. If you're trying to enter or grow in this market, that fact alone shapes every decision you make.

Flower, pre-rolls, and vapes together hold over 86% of Canada's cannabis market in 2025. Flower takes 32%, pre-rolls take 33%, and vapes take 21%. The remaining 14% is split across edibles, concentrates, topicals, and other formats.

I find the pre-roll number especially interesting. Pre-rolls are now the single largest category in Canada — bigger than flower itself. That's a shift that happened fast, and it tells you something real about what consumers want: convenience over customization.

What does this concentration mean for market strategy?

When three categories hold 86% of a $4.1 billion market, the math gets simple and brutal at the same time.

The opportunity is large, but so is the competition.

Here's how I think about it:

| Category | Market Share | What It Signals |

|---|---|---|

| Pre-roll | 33% | Convenience is king; consumers want ready-to-use |

| Flower | 32% | Core users still exist; the traditional base holds |

| Vape | 21% | Fast-growing tech-forward segment; high margin potential |

| Other (edibles, etc.) | 14% | Fragmented; harder to scale; niche-specific |

The vape segment at 21% is the one I watch most carefully. It's the youngest of the three dominant categories, and it's still growing. The regulatory environment in Canada shapes vape products in ways that are unique to this market — which I'll go into next.

Pre-rolls winning the top spot isn't just a convenience story. It also reflects how retail has matured. When consumers can walk into a licensed store and pick from 50 pre-roll SKUs, the friction of rolling your own disappears. Brands that built early in pre-rolls now have the shelf space and the consumer trust that's hard to displace.

Flower holding steady at 32% tells me the core cannabis user hasn't gone anywhere. But the growth vector in this category is slowing. Flower will remain a base, not a growth driver.

What Does the Canada Cannabis Vape Market Actually Look Like in 2025?

Vape is the most technically shaped segment in Canada. Federal rules set a hard ceiling on THC per package, and that ceiling changes everything — the product formats, the sizes, and the brands that win.

Canada caps THC at 1,000mg per single vape package. Because of this, the market is concentrated in 1g formats (and near-1g sizes like 0.95g and 1.2g). Cartridges lead at roughly 75% market share, with disposables at 25% — but disposables are climbing fast.

The disposables growth story is the one I keep coming back to. From 9.6% in 2023 to 29% by end of 2025, this kind of growth is really quite rapid and has tremendous potential.

Who are the top brands in Canada's vape market?

The brand landscape in Canadian vapes is clear at the top, with real separation between the cartridge and disposable leaders.

Top 10 Cartridge Brands (2025):

| Rank | Brand |

|---|---|

| 1 | Spinach |

| 2 | Boxhot |

| 3 | General Admission |

| 4 | XPLOR |

| 5 | Tribal |

| 6 | Sticky Greens |

| 7 | DEBUNK |

| 8 | Weed Me |

| 9 | Adults Only |

| 10 | Endgame |

Top 10 Disposable Brands (2025):

| Rank | Brand |

|---|---|

| 1 | Back Forty |

| 2 | Boxhot |

| 3 | General Admission |

| 4 | Kolab |

| 5 | Papa's Herb |

| 6 | Spinach |

| 7 | XPLOR |

| 8 | Vox |

| 9 | SUPER TOAST |

| 10 | DEBUNK |

A few things jump out at me from these lists.

First, Boxhot, General Admission, XPLOR, Spinach, and DEBUNK appear on both lists. That means these brands have built enough operational and brand strength to compete in two formats at once. That's not easy. It requires different supply chains, different retail positioning, and different consumer messaging.

Second, the disposables list has different top brands than the cartridge list. Back Forty sits at number one in disposables but doesn't appear on the cartridge list at all. They chose a format and went all-in on it. That's a valid strategy and it's working for Back Forty.

Third, the 1,000mg THC cap creates an interesting dynamic. In markets without this cap, you see much larger disposable formats — 2g, 3g, even 5g. In Canada, every brand is working with the same size constraint. Differentiation has to come from oil quality, hardware feel, and brand identity. That levels the playing field in some ways and makes it harder in others.

The rise of disposables also maps to a broader consumer behavior shift. Newer and occasional cannabis users prefer disposables. They're lower commitment — no charger needed, no cart to buy separately. As Canada's legal market matures and reaches more mainstream consumers, disposable growth makes complete sense.

What's Happening in Canada's Cannabis Oil Market in 2025?

Oil type is where I see the most dramatic shift in Canada right now. This is a story about consumer taste evolving faster than many brands expected, and about a new format taking over from what was once the default.

Starting in early 2025, distillate's market share began dropping quickly. Liquid diamond is rising fast enough that it may surpass distillate soon. Live resin is also growing, though at a slower pace.

This shift matters because oil type is one of the main ways consumers compare products. A consumer who has tried liquid diamond is unlikely to go back to distillate voluntarily. The sensory gap is real.

Why is liquid diamond replacing distillate in Canada?

Understanding this shift means understanding what each oil type actually is and what it delivers to the consumer.

| Oil Type | Production Method | Flavor Profile | Consumer Perception |

|---|---|---|---|

| Distillate | High-heat extraction; removes most terpenes | Mild, neutral | Entry-level; affordable; consistent |

| Live Resin | Extracted from fresh-frozen cannabis; preserves terpenes | Rich, complex, strain-specific | Premium; enthusiast-preferred |

| Liquid Diamond | THCA crystals dissolved in terpene sauce | Very clean potency + strong flavor | Newest premium tier; fast-growing |

Distillate built the vape market in Canada. It was cheap to produce, consistent to work with, and easy to put into hardware. For a new legal market trying to get products onto shelves and prices down, distillate made sense. It was the practical choice.

But consumer education has moved faster than most brands expected. Canadian cannabis buyers in 2025 are not the same buyers from 2019. They've tried more products. They've read more. They know what terpenes are. They can taste the difference.

Liquid diamond sits in a specific place: it delivers higher apparent potency (because THCA crystals are highly concentrated) while also carrying strong flavor from the terpene sauce it's suspended in. For a consumer who cares about both — and more of them do now — liquid diamond wins on both dimensions.

Live resin's slower growth makes sense too. It's harder to produce, requires fresh-frozen starting material, and costs more at every step. But it has a loyal base of consumers who value the full-spectrum experience. It will keep growing, but it won't grow as fast as liquid diamond because the price ceiling on live resin is lower than on liquid diamond in most retail environments.

The brands that moved into liquid diamond early — or that can transition their oil supply now — are in a better position for the next two years. The brands still heavily invested in distillate infrastructure face a harder decision.

Conclusion

Canada's $4.1B cannabis market in 2025 is concentrated by province, dominated by three product types, and in the middle of fast shifts in both vape formats and oil types. The brands that understand these moves will lead.