Michigan Cannabis Market Report 2025: What Happened in This Market?

The Michigan cannabis market just hit a wall. Sales dropped for the first time since legal adult use launched. If you sell vape products there, this report is the signal you cannot ignore.

Michigan's adult-use cannabis market brought in roughly $3.17 billion in 2025. That is a 3.1% drop from 2024's $3.27 billion. It is the first annual decline since recreational sales started in 2019. The main driver is simple: prices kept falling, but sales volume did not grow fast enough to make up the difference.

I have been watching the Michigan market closely, and this report pulled together everything I needed to understand what is actually happening on the ground. Let me walk you through the data, because the story is more nuanced than just "sales are down."

How Do Cannabis Product Categories Stack Up in Michigan in 2025?

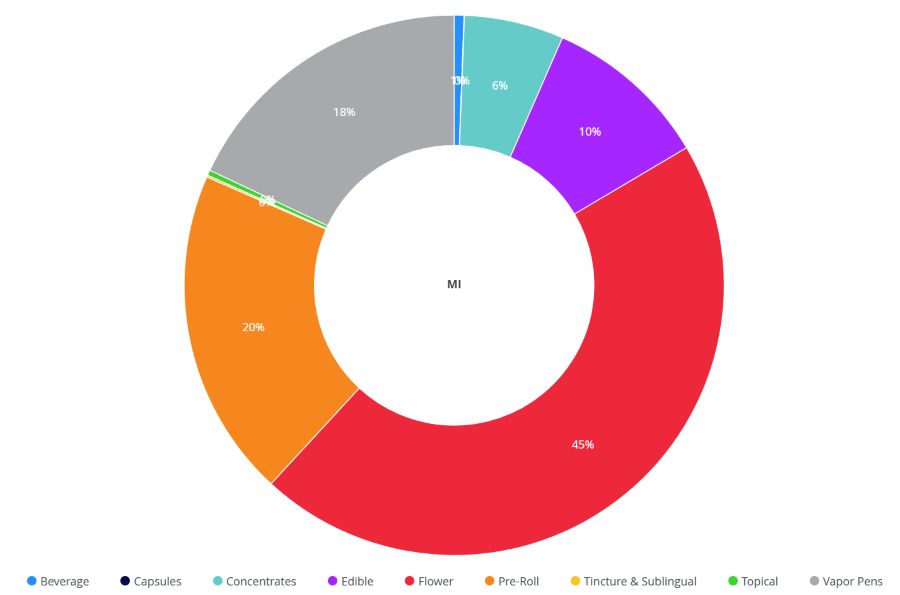

Flower still dominates, but not everything is holding its ground. If you are allocating production resources, you need to know exactly where the demand is sitting right now.

In Michigan's 2025 cannabis market, flower holds the largest share at 45%. Prerolls come in second at 20%. Vape products sit third at around 18%. Edibles make up 10% and concentrates take the remaining 6%.

Michigan's 18% vape share stands well below the national average of 25%. That gap is significant. Here is a closer look at how the categories compare:

| Product Category | Michigan Market Share | National Average (Approx.) |

|---|---|---|

| Flower | 45% | ~40% |

| Preroll | 20% | ~14% |

| Vape | 18% | ~25% |

| Edibles | 10% | ~12% |

| Concentrates | 6% | ~6% |

The vape underperformance in Michigan is worth paying attention to. One major factor is price compression. Michigan has some of the lowest cannabis prices in any legal state. When prices drop to extreme lows, consumer behavior shifts. Some buyers trade up to concentrates for perceived value-per-dose. Others stick with flower, which remains the most familiar format. Vape products occupy a middle ground that gets squeezed when the market races to the bottom on price. That said, the vape category is still the third-largest in the state, and its hardware requirements are very specific. Brands that can compete on price without gutting their hardware quality will likely hold or grow their slice of that 18%.

What Is the Current Price Level for Cannabis Vapes in Michigan?

Michigan has built a reputation for having the lowest cannabis prices of any legal state in the US. That reputation is now stretching into uncomfortable territory for brands and operators.

Michigan's average retail price for a cannabis vape in 2025 is approximately $9.87. Products priced below $5 now account for more than 20% of the market. This is the lowest pricing environment among all legal cannabis states, in some cases undercutting even illicit market prices in other regions.

Will Michigan Vape Prices Keep Falling, or Have We Hit the Floor?

I think Michigan is close to its pricing floor, but not quite there yet. Here is how I see it breaking down:

| Price Tier | 2024 Market Presence | 2025 Market Presence |

|---|---|---|

| Under $5 | Minor share | 20%+ of products |

| $5–$10 | Dominant tier | Still major, but shrinking |

| $10+ | Moderate | Declining share |

Starting in 2026, Michigan introduced new cannabis-specific taxes. That pushed prices up slightly in the short term. I have seen this play out in other markets. A tax increase creates a temporary price floor. But over 12 to 24 months, competitive pressure tends to erode it again as brands absorb costs rather than lose shelf space.

The difference in Michigan is that prices have already fallen so far that the margin for further drops is genuinely thin. A distillate vape cannot be produced, filled, packaged, distributed, and taxed for $3 and still generate any profit. At some point, the market stabilizes not because demand changes, but because the supply side cannot physically go lower. We are approaching that point. Brands entering Michigan should plan for a sustained low-price environment rather than betting on a recovery. Build your cost structure around that reality from day one.

What Does the Michigan Vape Market Actually Look Like Right Now?

The format split and size trends inside Michigan's vape category tell a very different story from the rest of the US. If you are designing hardware or planning SKUs for this market, these numbers matter a lot.

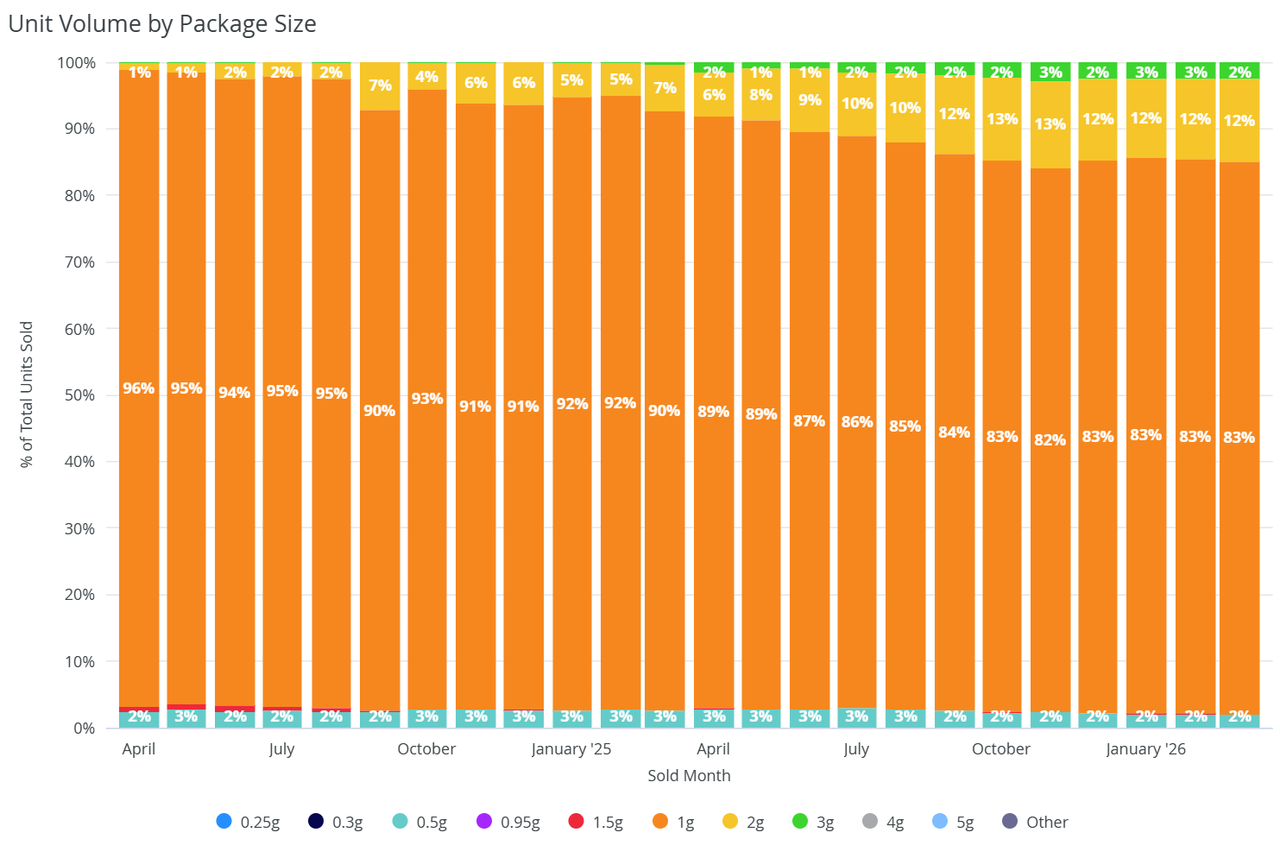

Michigan's vape market is split between 510 cartridges at 53.7% and disposables at 46.3%. The market is moving strongly toward larger capacities. Michigan is more aggressive on this trend than most other states, with 1g products dominating, 2g already at 12%, and 3g products appearing at around 3%.

Why Is Michigan Moving to Larger Vape Sizes Faster Than Other States?

Price compression is the main driver. When a 1g vape retails for under $10, the consumer mindset shifts. A 2g product at $15 or $16 feels like strong value. Consumers are not just buying cannabis. They are buying perceived savings. Here is how Michigan's size distribution compares to general US market trends:

| Vape Capacity | Typical US Market | Michigan 2025 |

|---|---|---|

| 0.5g | Moderate share | ~2% only |

| 1g | Dominant tier | Dominant tier |

| 2g | Emerging / growing | ~12% |

| 3g | Rare / niche | ~3% |

Michigan's 0.5g share of roughly 2% is striking. In most states, 0.5g products still hold a meaningful portion of the market, often serving entry-level or trial buyers. In Michigan, that format has been almost entirely phased out. Consumers here are experienced, price-conscious, and buying in quantity. The trajectory points clearly toward 2g continuing to grow its share through 2026. At Transpring, we have seen demand for 2g hardware increase steadily from our brand customers. The Michigan data confirms what we are already hearing from the market. Brands planning new SKUs for Michigan should prioritize 1g and 2g formats and consider whether 3g is the next frontier worth exploring, especially as the price-per-mg math continues to drive buying decisions.

Which Oil Types Are Winning in Michigan's Vape Market?

Oil type preferences shape hardware requirements directly. The oil that leads the market determines the coil technology, viscosity handling, and leak resistance your device needs to support.

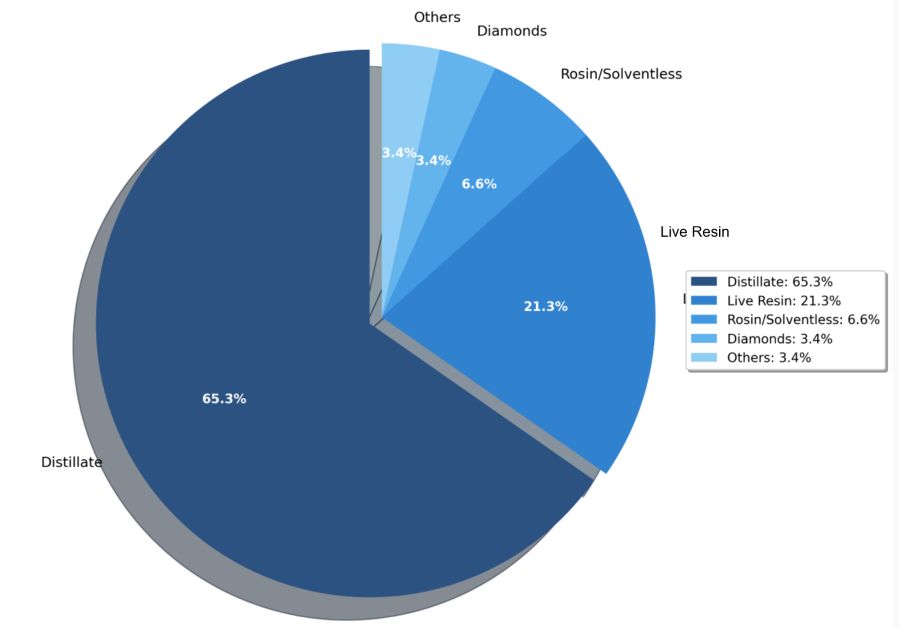

Distillate leads Michigan's vape oil market at 65.3%. Live Resin is second at 21.3%. Live Rosin holds third place at 6.6%. The remaining share is split across other oil types.

What Does Michigan's Oil Mix Mean for Hardware Selection?

Each oil type creates different hardware demands. Understanding this helps brands choose the right device and avoid the most common compatibility failures.

| Oil Type | Michigan Share | Key Hardware Requirement |

|---|---|---|

| Distillate | 65.3% | Standard viscosity, wide coil compatibility |

| Live Resin | 21.3% | Higher viscosity tolerance, consistent heating |

| Live Rosin | 6.6% | Solventless, requires precise low-temp control |

| Other | ~6.8% | Varies by formulation |

Distillate's dominance at 65.3% is not surprising. It is the most cost-effective oil to produce at scale, and in a price-sensitive market like Michigan, that matters enormously. Brands using distillate can hit lower price points and still work with a wide range of hardware options. Live Resin's 21.3% share is meaningful. This segment is growing nationally, and Michigan's market reflects that. Live Resin requires hardware that can handle thicker viscosity without clogging and deliver consistent heat to preserve terpene profiles. Cheap hardware fails here. Live Rosin at 6.6% is the premium tier. Consumers buying Live Rosin are not hunting for the lowest price. They are paying for purity and flavor. This is where hardware quality becomes a brand differentiator. A poorly performing device damages the perception of a premium oil more than any other category. For brands operating across all three oil types, I recommend treating hardware selection as a category-specific decision, not a one-size-fits-all choice.

Conclusion

Michigan's 2025 cannabis market is defined by falling prices, shifting formats, and a vape category that still has room to grow if brands approach it strategically.